Over the last 24–36 months, enterprise AI has shifted from scattered experiments to a competitive mandate — where the limiting factor is no longer access to models, but the ability to convert pilots into secure, governed, cost-disciplined production systems that move real KPIs.

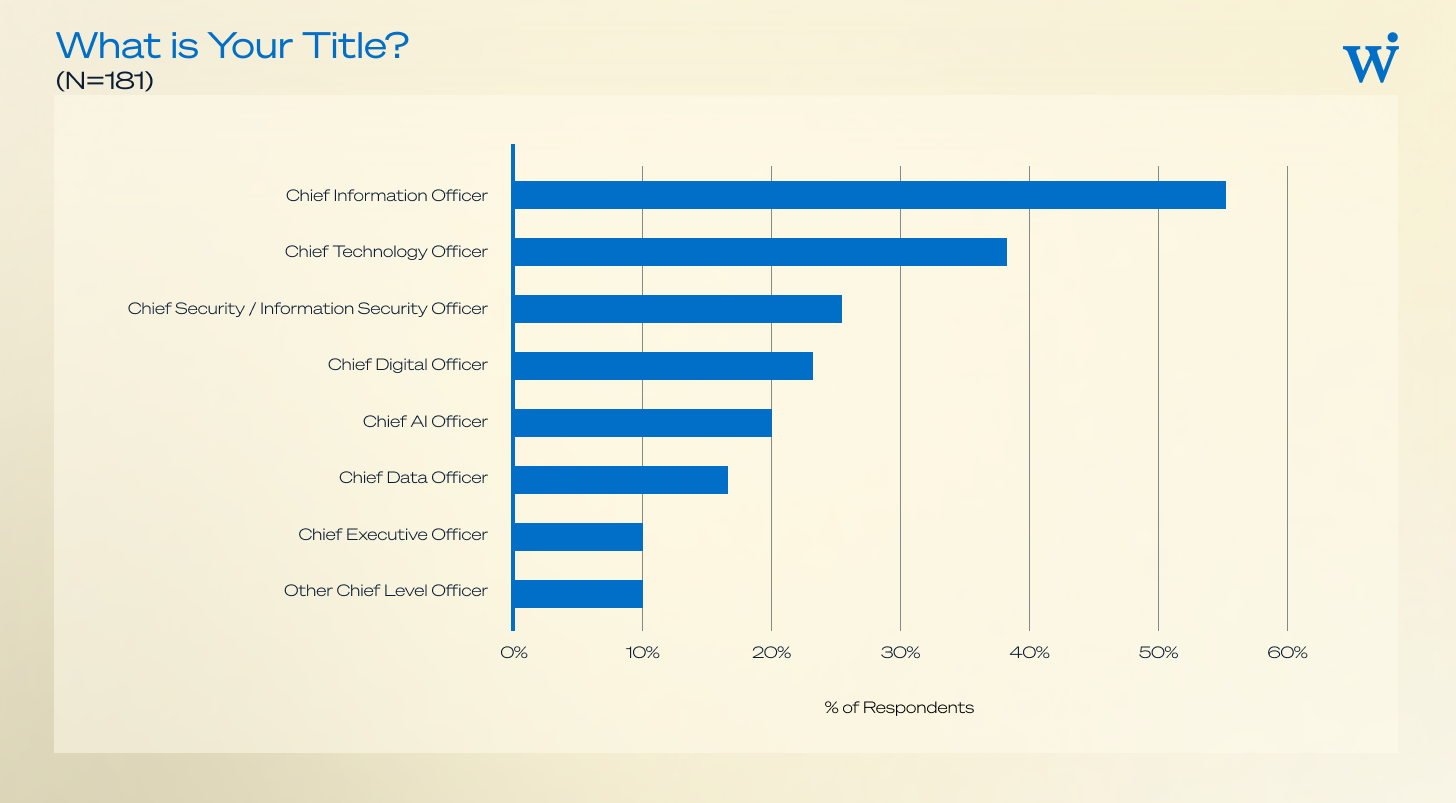

Drawing on direct input from 181 Chief-level technology, security, data, and AI leaders, we are excited to launch the inaugural Wing VC report on the State of AI in the Enterprise. Our report cuts through the hype to codify the ground truth of the AI supercycle: which deployments are scaling beyond productivity hacks, what’s stalling in the path to production, and how the platform landscape is actually forming within enterprise workloads.

Specifically, we find that:

- Enterprises expect a median of 50% of AI pilots to convert to production.

- 56% of large enterprises are in early or large scale production for AI agents. 32% are in large scale production for one or more AI use cases, and 24% are in large scale production for two or more use cases.

- OpenAI is the leader in large enterprise today. 61% of large enterprises rank OpenAI as #1 by AI workloads, while 17% rank Gemini as #1 and 11% rank Anthropic as #1.

- AI headcount reductions in affected teams will be meaningful. 66% of large enterprises expect that specific teams will experience headcount reductions of 10-25%.

- AI is not all hype. 72% of enterprises rank AI as squarely in-between hype and real.

- The widely publicized Project NANDA study (often referred to as the "MIT study" despite its tenuous association with the Institute) is, in our view, problematic. It received a lot of media attention despite widely recognized flaws. The data reported by our community of C-level executive respondents is notably more positive (and much more detailed).

The Wing VC report is uniquely based on direct feedback from 181 Chief Information, Technology, Security, Digital, Data, and AI Officers. 100% of respondents are chief-level officers. 52% of respondents are at large enterprises with 10,000 or more employees.

At Wing, we view the AI supercycle as a 10-20 year opportunity that’s still in its earliest innings. While there is fear of an AI bubble (which in certain over-capitalized sub-sectors is most likely justified), our analysis reveals a strong current of AI demand from enterprises across company sizes and industries. The AI results are not uniform. Many pilots do not convert, and many projects do not yet have a return on investment (ROI). But, many enterprises are seeing initial success, and this varied distribution of results is precisely what we would expect at this point in a supercycle.

In this post, we describe the 10 main findings from the Wing VC report. In addition, we include an appendix with additional findings for specific functions and industries.

Findings

1) 2026 will be the year of getting to production or generating value for many enterprises.

Many respondents are positive on AI in 2026. 35% said that 2026 will be the year of getting to production, generating value, or scaling. For example, when asked what they predicted for 2026, one Chief Data Officer (CDO) replied, "serious production use cases,” one Chief Information Security Officer (CISO) responded with "hockey stick adoption across nearly every aspect of corporate work,” while one Chief Information Officer (CIO) answered, "applied AI moving from hype to delivering real impact.”

Some respondents, however, are cautious. 12% expected a year of disappointment or a re-alignment of expectations from the current level of hype. For example, one Chief Technology Officer (CTO) predicted an "AI bubble reckoning," while one Chief Technology Innovation Officer (CTIO) thought AI would get a “reality check” in 2026. Meanwhile, two CIOs predicted AI would get “stuck in the mud,” and questioned if agents could actually “materially drive 25-30% ROI across the applications layer.”

Other respondents discussed specific capabilities they expected to see from AI this year; for example, a Chief Digital Transformation Officer (CDTO) discussed “agent swarms”. A few discussed states of mind; for example, one Chief Information and Digital Officer (CIDO) quipped, “courage.”

Overall, after mapping responses to a phrase cloud, we found a 3.3:1 positive-to-negative sentiment ratio. 103 respondents expressed positive expectations; 28 expressed neutral ones; and 31 expressed negative ones.

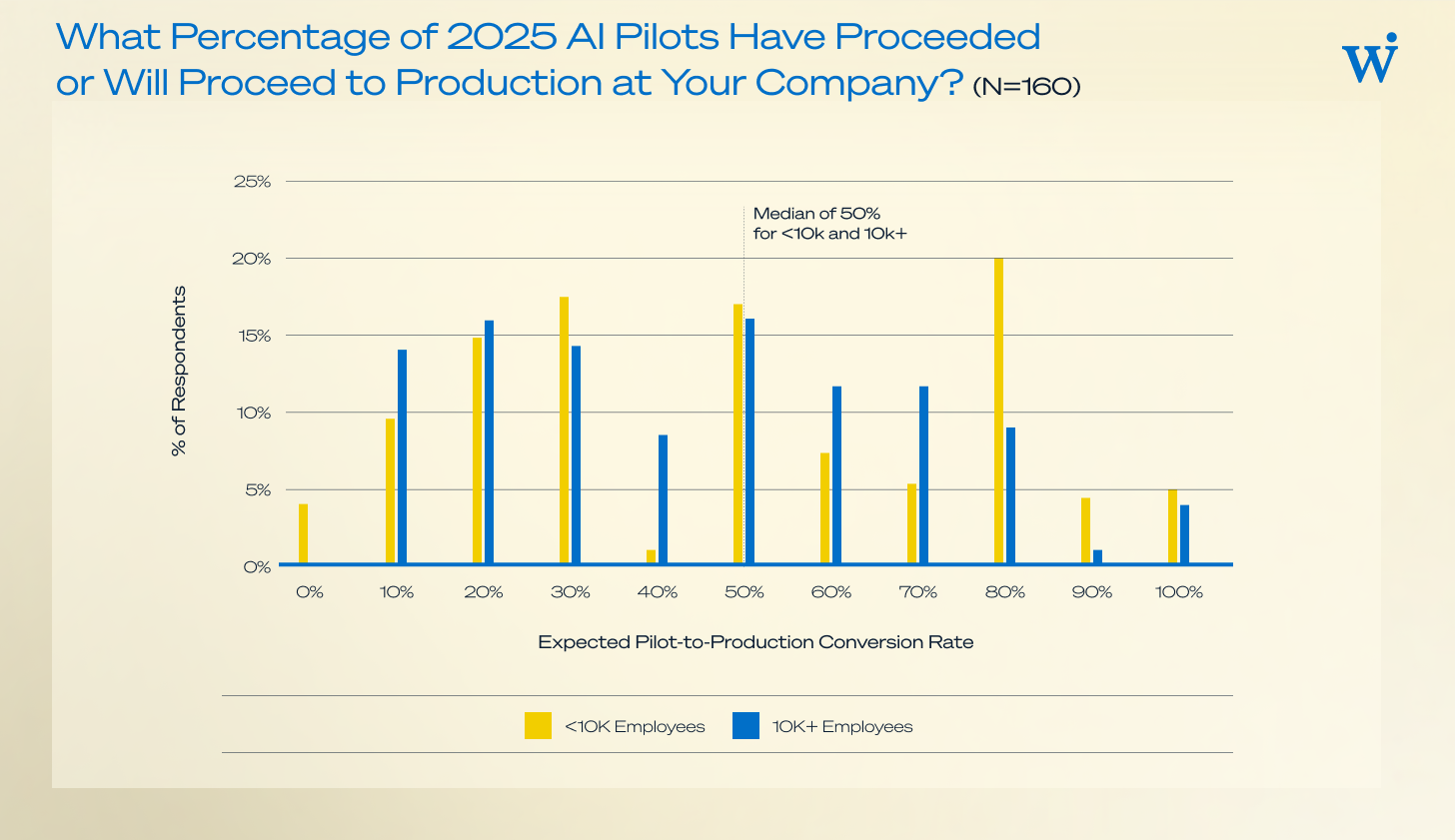

2) Enterprises expect a median of 50% of AI pilots to convert to production.

The median of 50% is the same for large enterprises (10,000+ employees) and small enterprises (less than 10,000 employees).

Large enterprises have two clusters: 41% expect a 10-30% conversion ratio, and 38% expect a 50-70% conversion ratio. The clusters reflect different strategies: letting a thousand blossoms bloom vs. focusing efforts on a few. For example, one CIO replied, “75%: we are careful on piloting to ensure value,” while another CIO replied, “we are running1000 experiments and some of those will bear fruit. 10% would be good.”

The results are a contrast to the takeaways from the MIT study, which in our view is confusing. In the MIT study, the survey questions as stated in the appendix (“How many GenAI pilots have been launched since Jan 2024? Of those, how many are now deployed at scale?”) do not seem to match the chart (which shows that 5% of embedded or task-specific GenAI are successfully implemented). They also do not seem to match the different findings (“only 5% of custom enterprise AI tools reach production,” “95% of organizations are getting zero return,” and “just 5% of integrated AI pilots are extracting millions in value.”) In our study, one Chief Data and AI Officer (CDAIO) even answered, in response to our AI pilot conversion question, “higher than [the] MIT study.”

3) 56% of large enterprises are in production for AI agents, and 53% of large enterprises report positive ROI on 2 or more AI use cases.

32% of large enterprises are in scale production with at least one AI use case, and 24% are in scale production for two or more AI use cases. Further, 68% of large enterprises report positive ROI with at least one AI use case, and 53% report positive ROI on two or more use cases.

These results are encouraging for startup founders across all application categories. While code generation is demonstrably a killer AI application, it is not the only one! We anticipate significant growth in the number of AI startups across application categories at large scale production over the next few years.

4) Customer service, software engineering, IT, and sales and marketing are the most significant functions for AI impact, followed by a broad array of other functions.

By company function, enterprises rank customer service, software engineering, and information technology (IT) as having the highest potential for AI impact. 71% of large enterprise respondents said customer service; 69% said software engineering; and 53% said IT.

Looking at specific pilots, respondents said sales and marketing, customer service, software engineering, assistants, and automation, respectively, are the most exciting for 2026.

Within sales and marketing, a CIO said “marketing content creation with legal and regulatory approvals for faster media campaigns,” a CTO said “narrative based personalization,” and a CDTO said “RCM [revenue cycle management] automation.” Within customer service, a CISO said, “customer service AI agents that can answer technical support questions or act without prompting to detect and correct potential customer impacting events.” Within automation, a CIDO said, “agents to improve performance and speed of processes that today take several human teams and often weeks to complete — down to a few minutes or less.”

Healthcare is a major industry vertical for AI pilots. For example, a CEO stated “ambient listening” and “radiology AI.” A Chief Artificial Intelligence Officer (CAIO) stated “ambient scribe” and “clinical/billing coding.” A CITO noted “structuring unstructured healthcare data.”

5) Enterprises described a wide range of insightful moonshot AI pilots and agents.

Agentic moonshot themes include: agentic organizations and agentic leaders, back office support, employee assistants, data management, finance functions, global good for humanity, insights, manual automation, and product development.

6) 61% of large enterprises rank OpenAI as #1 by the number of AI workloads, while 17% rank Gemini as #1, and 11% rank Anthropic as #1.

OpenAI is the leader in large enterprise today. 61% of large enterprises rank OpenAI as #1 by the number of AI workloads, while 17% rank Gemini as #1, and 11% rank Anthropic as #1. For small enterprises, Gemini’s and Anthropic’s positions are reversed. 65% of small enterprises rank OpenAI as #1, but 18% rank Anthropic as #1 and 8% rank Gemini as #1.

To be clear, OpenAI's lead is based on number of use cases, and not necessarily in overall usage. Some use cases, like coding, drive a lot more usage than others.

The results are a contrast to other publications which find that Anthropic is the market share leader in enterprise. It will be interesting to observe how the results change over time. We will likely learn more about the relative position and shifts among OpenAI, Gemini, and Anthropic in the enterprise over the next year.

Of note, “Other” ranks higher than the other named models in the survey. It could be that Alibaba’s Qwen is driving a meaningful number of the “Other” responses. We will add Qwen (and perhaps others) to future years’ surveys.

The following chart shows the average score of the respondents’ #1, #2, and #3 ranks. If a respondent ranked a model as #1, that response received a score of 3. If a respondent ranked a model as #2, that response received a score of 2. If a respondent ranked a model as #3, that response received a score of 1. All others had a score of 0.

Meta’s Llama, DeepSeek, and Mistral show up relatively more in the average score results, indicating that some respondents rank them as among the top three by the number of AI workloads.

7) RAG, agent/orchestration frameworks and vector databases are the most widely used tools and techniques.

Retrieval-augmented generation (RAG) is currently used by 76% of large enterprises, followed closely by agent/orchestration frameworks at 67%.

As a note, there is overlap between RAG, context engineering, and vector databases as terms. RAG and context engineering are vector database use cases. For the survey, we used all three terms to cast a wide net for respondents to identify with.

8) Integration and data are the two most important challenges to AI for large enterprises.

50% of large enterprises say that integration with existing systems is the most important challenge to AI at their companies, and 49% say that data is the most important challenge.

At small enterprises, data is the most important challenge with 54% of respondents, but security, governance, and privacy are the next most frequently mentioned, with 42% of respondents.

9) 66% of large enterprises expect headcount reductions of 10-25% for affected teams.

AI-driven headcount reductions in affected teams will be meaningful. 66% of large enterprises expect that certain teams will experience headcount reductions of 10-25% in 2026.

Importantly, our survey did not comment on the enterprise-wide net headcount impact from AI. Instead, we focused on the efficiency opportunities from AI, which highlights the displacement risk for certain talent categories.

At our private summit, we asked a Fortune 500 CEO, “What will be the net impact to your company’s headcount from AI?” His response? “Well,” he said, “It will be lower.” The degree to which it will be lower is to be determined.

10) 72% of enterprises rank AI as squarely in-between hype and real.

AI is not all hype. On a scale of 1 (hype) to 6 (real), 72% of enterprises rank AI as a 3 or 4.

This finding corresponds with the above findings on 2026 expectations, projected pilot-to-production conversion, and ROI. There is a strong current of demand for AI within large enterprises.

%20to%206%20(Big%2C%20Real%2C%20and%20Now)_.png)

Conclusion

AI is the next multi-decade supercycle, and our research indicates a strong current of demand, with early signs of success. We are excited to partner with founders building this next generation of technology. We hope that the report shares practical insights from the perspective of buyers, and we look forward to your thoughts and reactions. Reach out to us on X or LinkedIn!

Methodology

The Wing VC report is based on our exclusive Enterprise Technology Leadership Network. The study was conducted between October 10, 2025 and October 14, 2025 in conjunction with Wing Summit 2025. The summit is known as the Davos for CXOs, and summit participants include chief information officers, chief technology officers, chief security officers, chief digital officers, chief AI officers, chief data officers, and board members and chief executive officers.

The Wing Enterprise Technology Leadership Network is a unique and critical attribute to the study. The report is conducted directly with 181 enterprise executives. 100% of respondents are chief-level officers. 52% of respondents are at large enterprises with 10,000 or more employees, and 48% of respondents are at small enterprises with 5,000 to 9,999 employees.

We would like to recognize and thank Wing partners Chris Zeoli, Tanay Jaipuria, and Sam Parker for their significant contribution to the design and insights of the report. In addition, thank you to Wing consultant Clayton Ramsey for his significant contribution to the data and analyses.

Notes on the Project Nanda Study

In July 2025, some individuals associated with Project NANDA — a decentralized industry project which originated at MIT but is not administered or managed by it — published “The GenAI Divide: State of AI in Business 2025." The report instantly went viral for its central claim that 95% of AI pilots fail, a statistic that was repeated by news organizations ranging from Axios to Fortune. However, since the report’s publication, numerous industry analysts and researchers have pointed out several significant methodological flaws that suggest the "failure" is overstated and the data is non-representative. Kevin Werbach, Professor and Chair of Legal Studies & Business Ethics at the Wharton school, wrote that he found the NANDA report “deeply problematic,” citing issues of confirmation bias and finding no credible support for its conclusions. Other analysts have also noted that the report’s findings are biased towards the authors’ own commercial solutions and are not based on the analysis or methodology.

Appendix

61% of large enterprises have 10 or more AI apps or agents.

Enterprises have a median of 7.25 AI apps or agents. Large enterprises have a median of 10, and medium enterprises have a median of 5. For example, one large enterprise CDIO said, “21 agents launched out of 72 agents in the pipeline.” A large enterprise CXO said, “AI applications: 25, Agents: none.” A large enterprise CIO said, “We have created 500+ agents and have created a digital core from which to organize data.”

65% of large enterprises expect a reduction in SaaS spend or SaaS vendors due to AI.

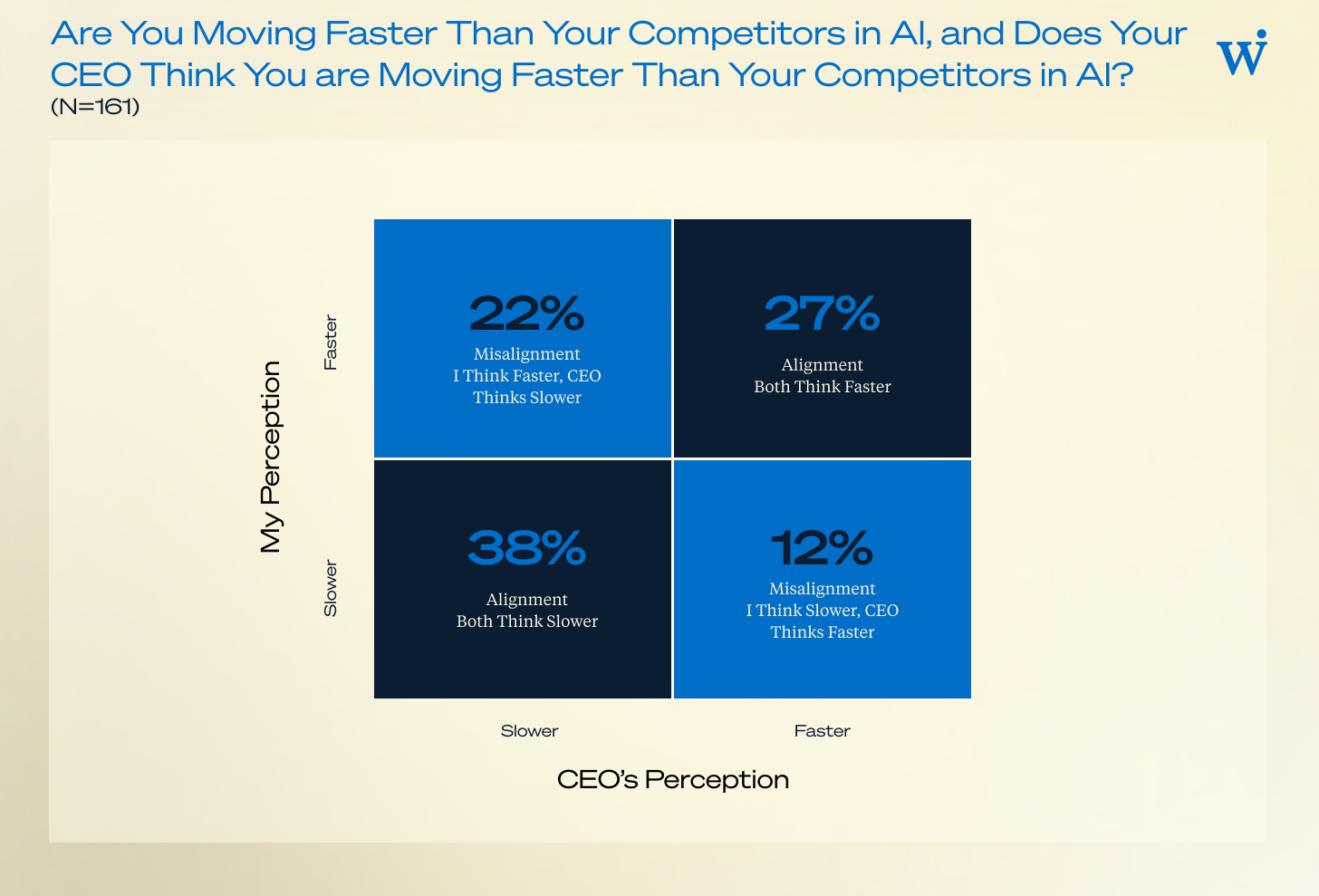

50% of CXOs think they are slower in AI than their competitors, and 61% of CXOs think their CEOs think they are slower in AI than their competitors.

For CDOs, AI has created the most value in customer channels of call centers and chat/email-based communications.

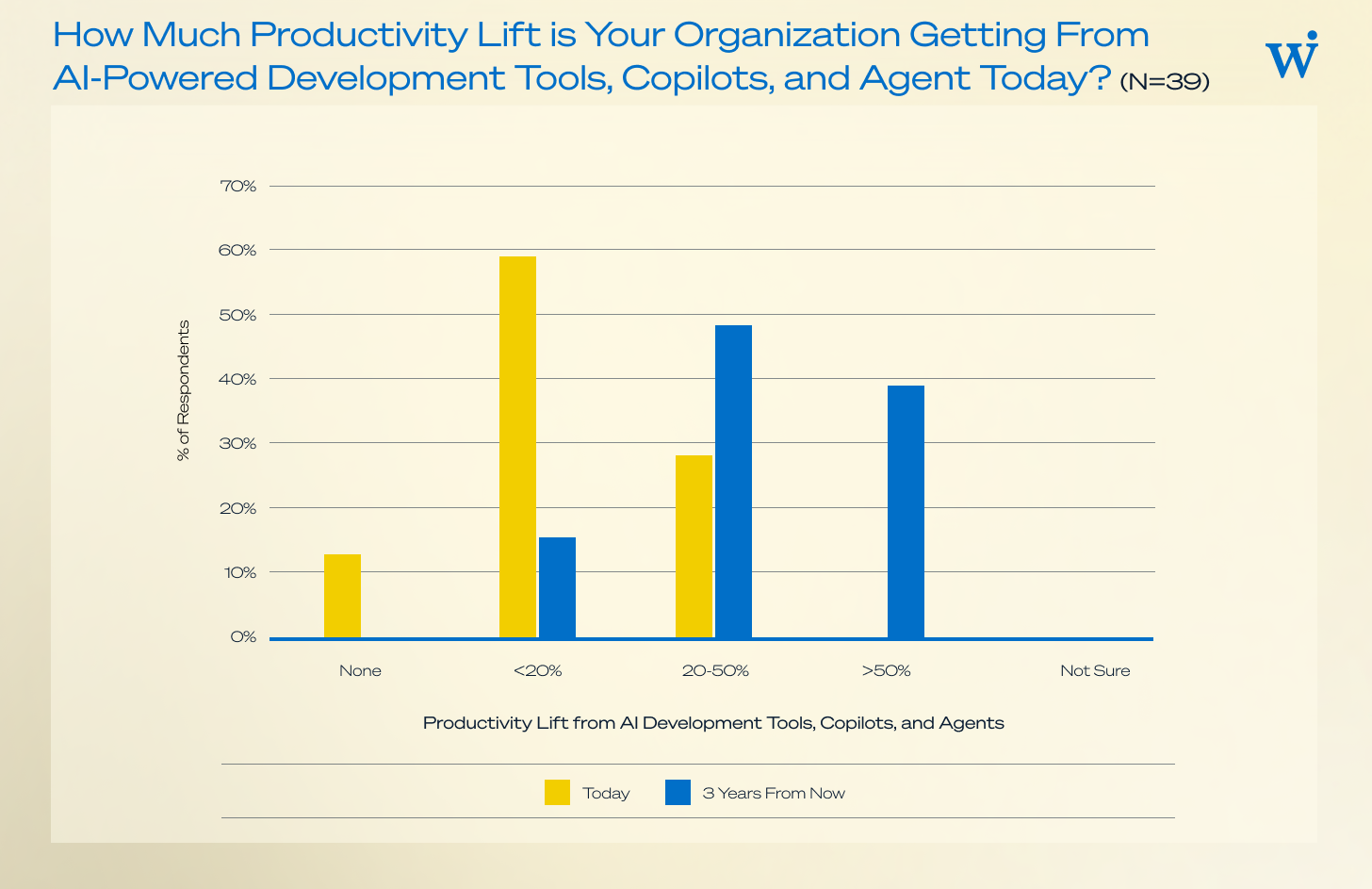

For CTOs, 87% have productivity lift today from AI development tools, copilots, and agents. 28% have productivity lift of 20%-50% today!

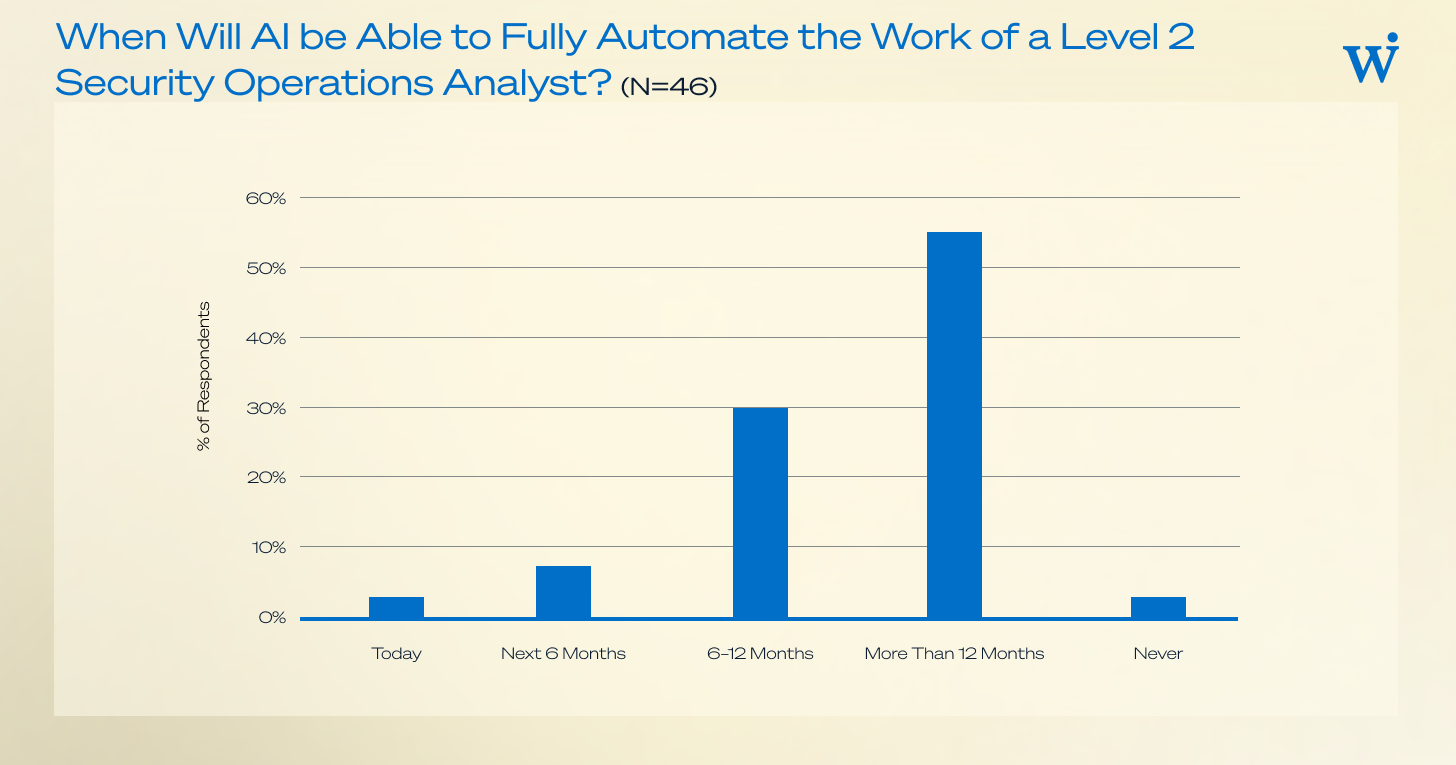

For CISOs, 41% expect Level 2 SOC analyst automation within 12 months, and only 22% rank their risk and governance posture as very good or solid.

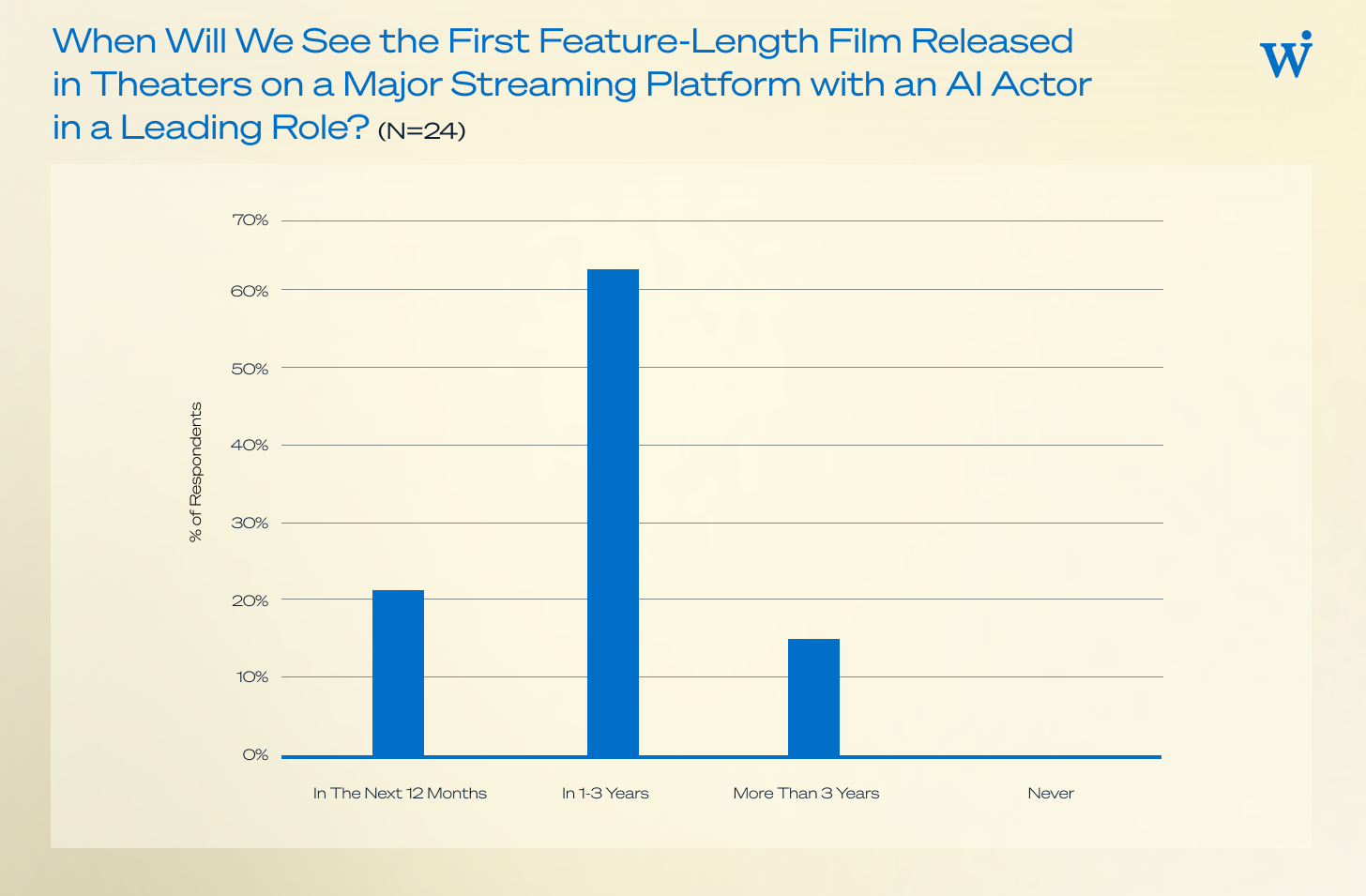

Within the media industry, executives favor AI text significantly over AI images, video, and audio currently, and 83% expect an AI actor in a leading role within 3 years.

Within financial services, customer engagement & personalization and fraud & risk will be the most transformative AI use cases, and 52% of respondents indicate that automating trading and financing decisions is challenging or far into the future.

.avif)