Welcome to Wing's seventh annual V21 study!

Each year, we examine the earlystage startup funding dynamics among the industry's highest-quality startups. We analyze the trends and characteristics of companies invested in by at least one of 21 elite venture capital firms, the "V21." Our purpose is to separate the signal from the noise in venture market data and provide insights to founders building companies and raising earlystage capital. This year, the curated V21 dataset captures the details of 11,381 deals at 5,598 companies invested in by V21 firms at Seed, Series A, and Series B stages from 2010 to 2023.

Last year, we observed that 2022 was the "year of living cautiously." V21 firms' deal volume decreased materially from the unprecedented levels of 2020 and 2021. As the pool drained, the number of Cannonball Effect financings crashed with a thud. And, Series A and Series B financing sizes and pre-money valuations experienced significant quarter-to-quarter declines. We asked in the study, "how much of a reset are we in" and "how long will it last"?

Today, we are in a time of "market divergence", in which companies in the fast-moving water of AI have seemingly insatiable demand for AI startup funding, while those perceived to be in the back-eddies of prior technology cycles can find themselves to be almost unfinanceable. This year's V21 study reveals that overall deal volume has bottomed out and may be showing signs of renewal, driven by increases in generative AI and some closely-related sectors. When we take a closer look at these generative AI companies, it is interesting to observe some characteristics that are distinctly different from their non-generative AI peers.

In this study:

Executive summary · V21 firms' deal volume · Cannonball Effect · Financing size · Jumbo Series A's · Pre-money valuation · Round number · Cumulative capital raised prior to round · Years since founding · Revenue generation · Time Machine analysis · Methodology update · FAQ · Conclusion

Executive summary

The investment pace for V21 firms bottomed out in 2023 and may be showing some weak signals of modest growth. The number of first-time V21 Seed, Series A, and Series B quarterly deals peaked at 211 in 2Q21. For the past four quarters, the number has been relatively flat — from 102 in 4Q22 to 103 in 4Q23.

The venture cycle has had a significant impact on Series As and Series Bs, but Seeds have generally been more resilient.

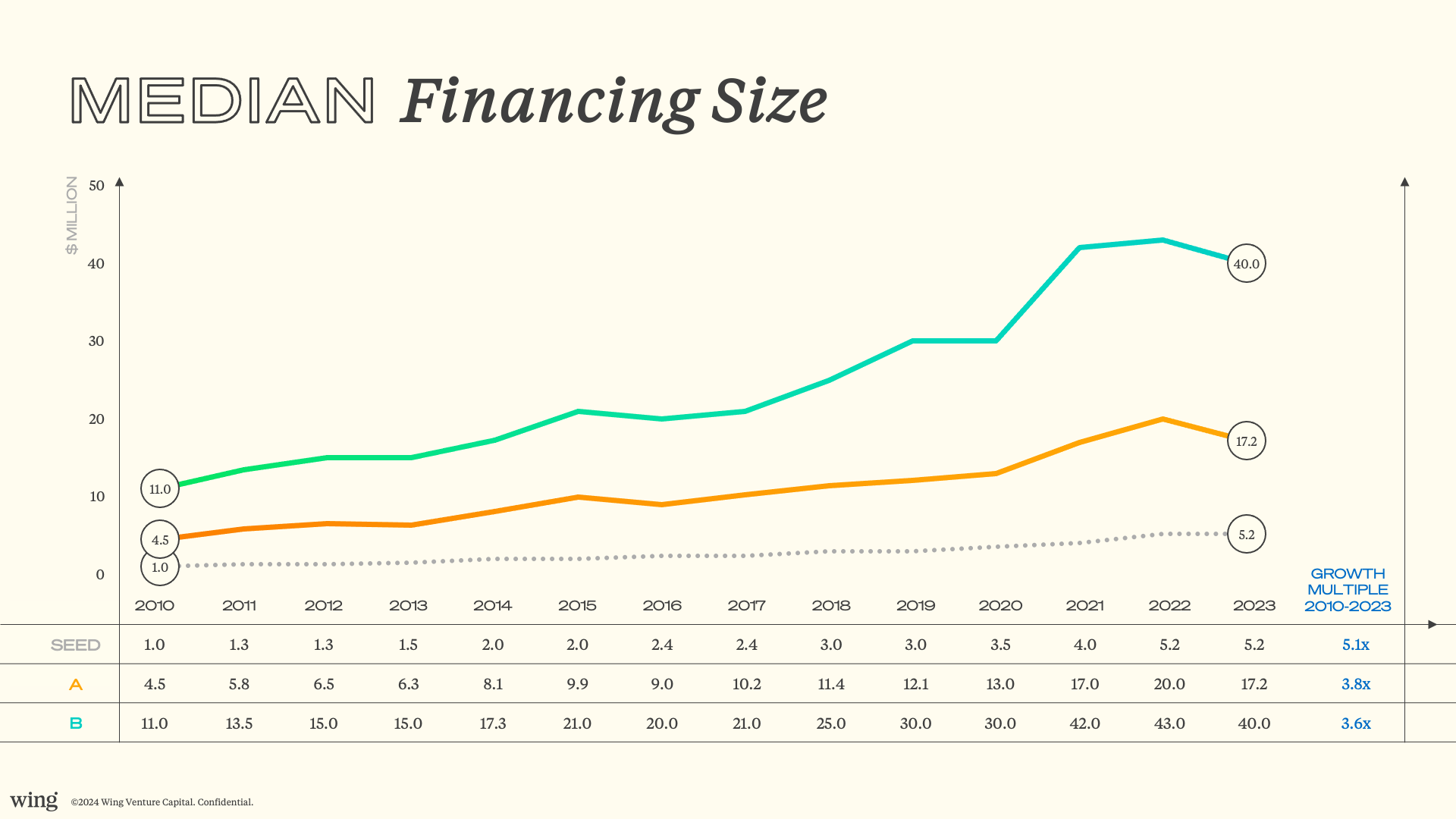

- For Seeds, the median financing was $5.2M in 2023, unchanged from the prior year, and the median pre-money valuation was $17M in 2023, down 3% from the prior year.

- For Series As, the median financing was $17.2M in 2023, down 14% from the prior year, and the median pre-money valuation was $48M in 2023, down 20% from the prior year.

- For Series Bs, the median financing was $40M in 2023, down 7% from the prior year, and the median pre-money valuation was $160M in 2023, down 30% from the prior year.

Quick-reference benchmarks

Stage | Median financing size (2023) | Median pre-money valuation (2023) | YoY change (valuation) |

|---|---|---|---|

Seed | $5.2M | $17M | −3% |

Series A | $17.2M | $48M | −20% |

Series B | $40M | $160M | −30% |

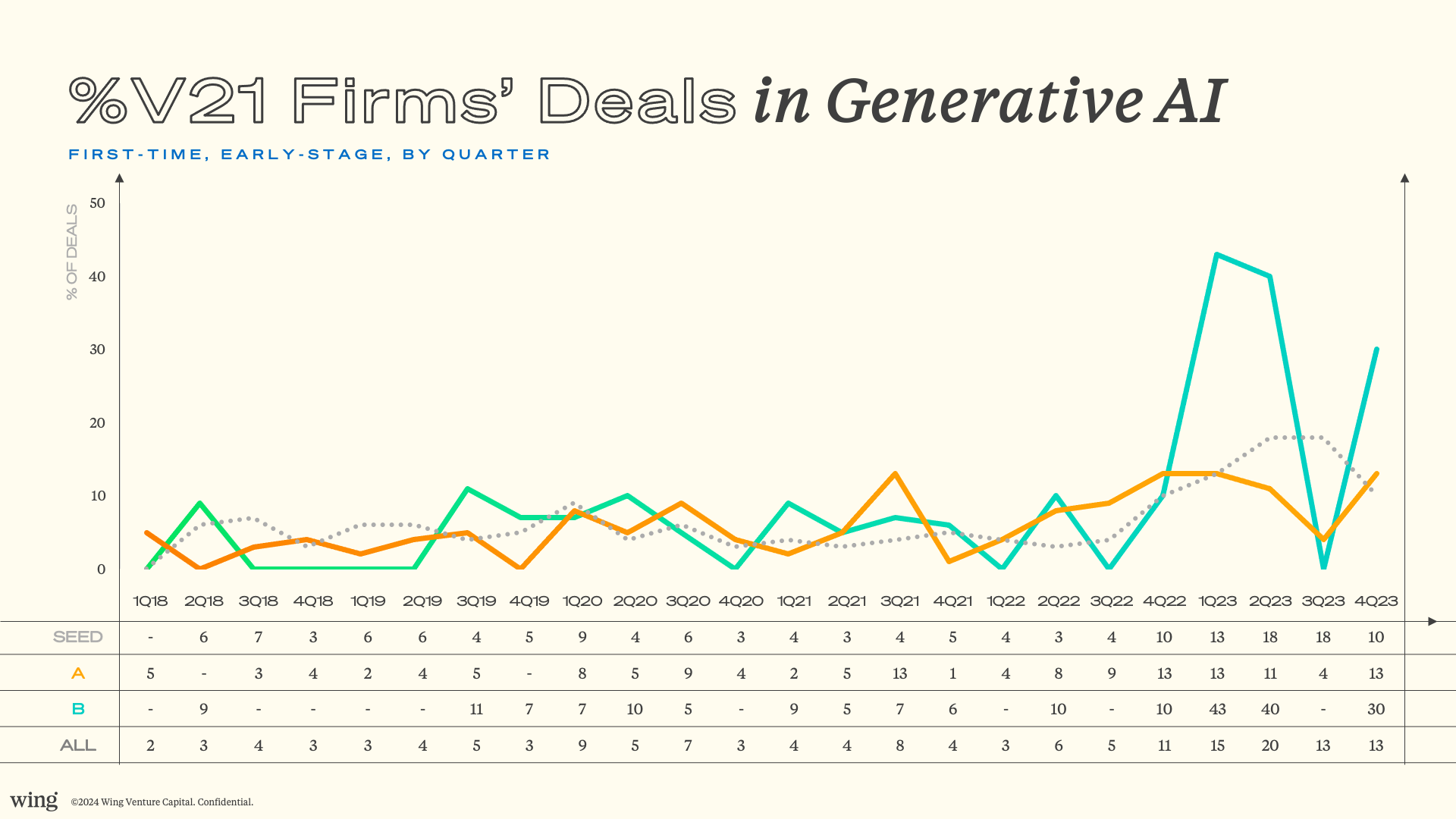

Generative AI continues to increase significantly. 15.1% of first-time V21 investments (i.e., not a follow-on investment in a company where the firm had previously invested) in Seed, Series A, and Series B deals were in generative AI in 2023, up from 5.6% in 2022.

The market divergence is evident in the characteristics of generative AI vs. non-generative AI companies. Generative AI companies have higher median deal sizes and valuations, are younger, and are more likely to still be in their pre-revenue phase, than their non-generative AI peers.

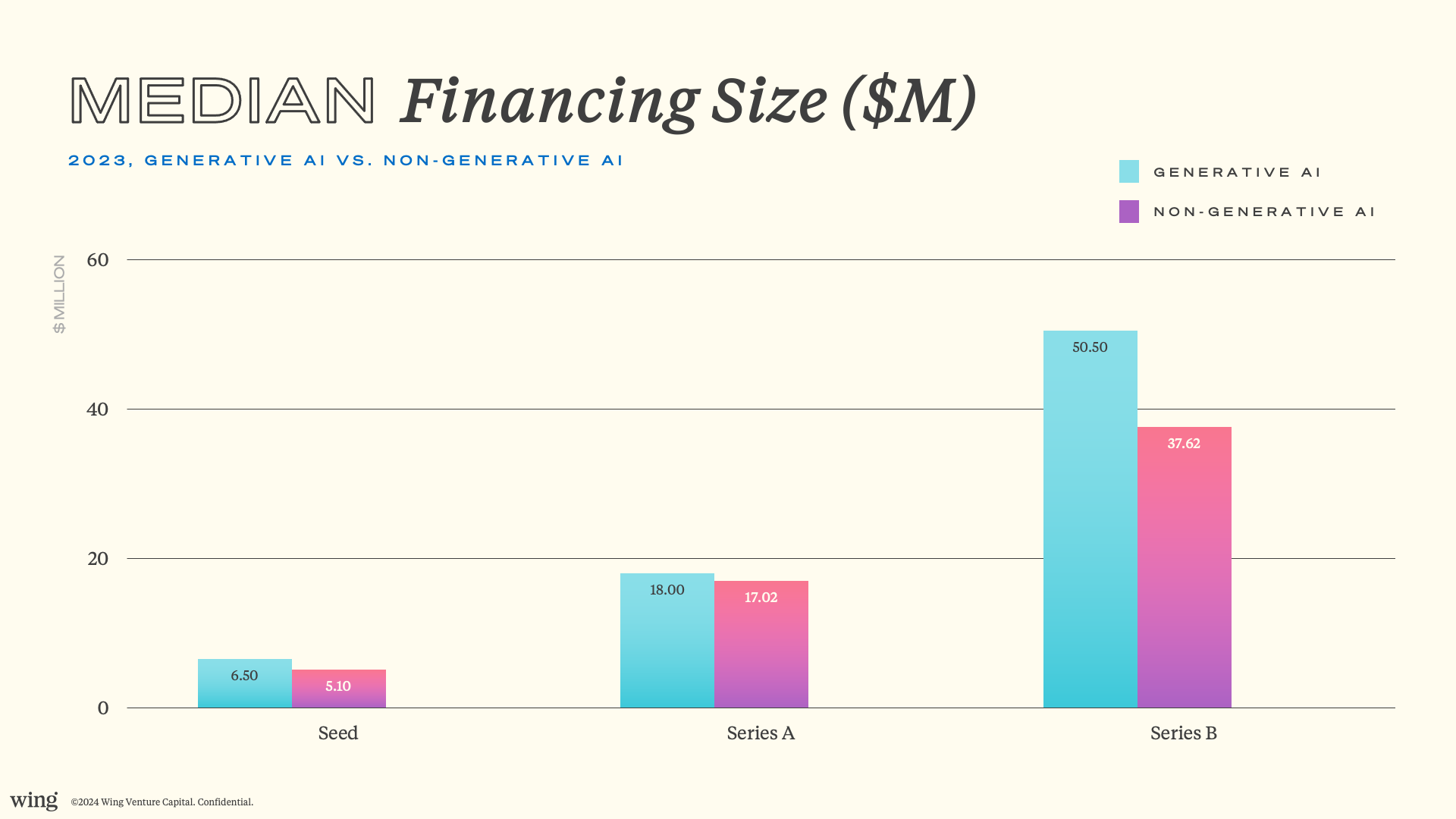

- Generative AI companies have median financing sizes 27% larger than non-generative AI companies at Seed, 6% larger at Series A, and 34% larger at Series B.

- Generative AI companies have median pre-money valuations 69% larger than non-generative AI companies at Seed, 217% larger at Series A, and 215% larger at Series B.

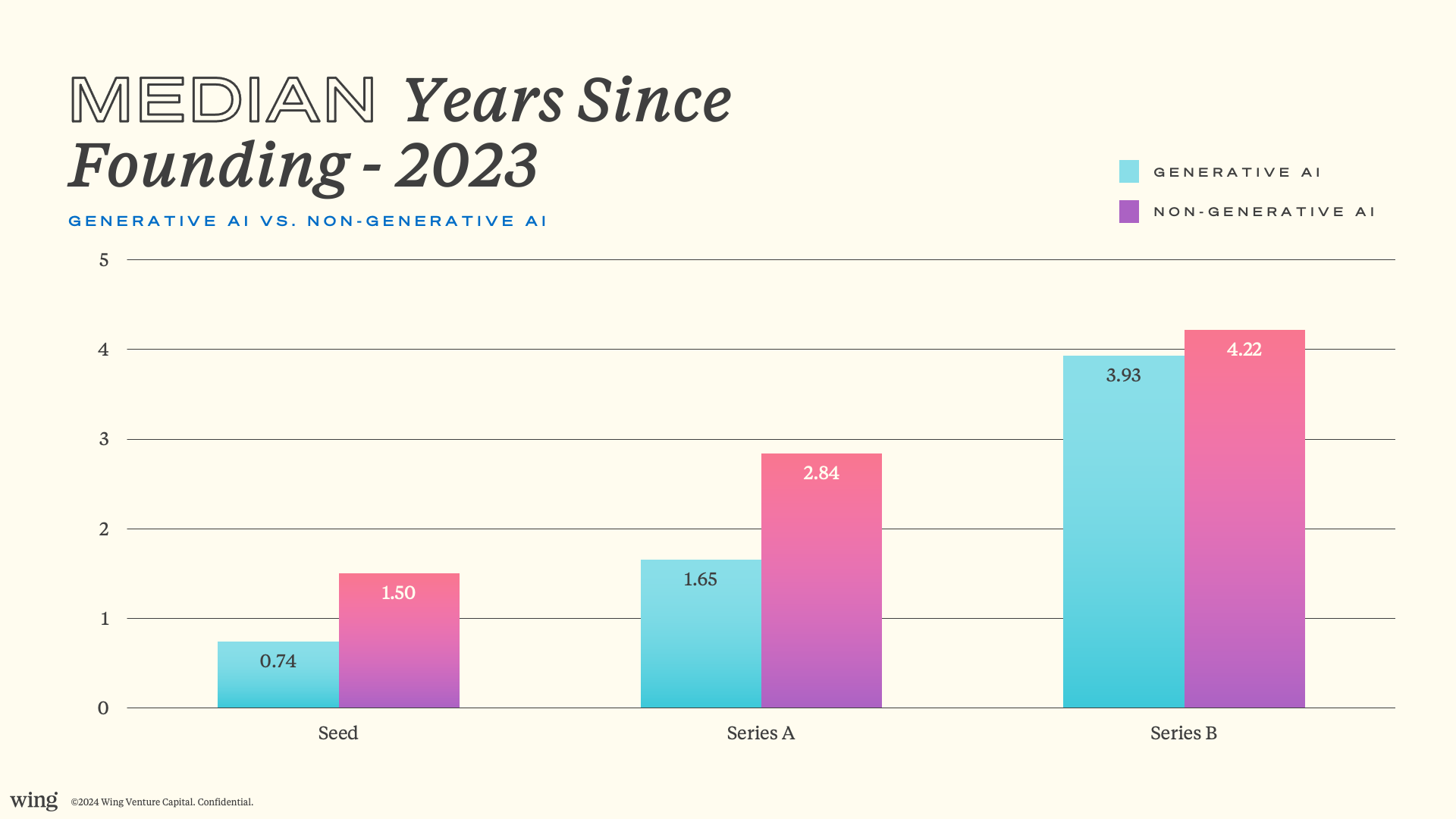

- Generative AI companies receiving Seed financings in 2023 had a median age of 0.7 years since founding, versus 1.5 years for non-generative AI companies.

- Generative AI companies receiving Seed financings in 2023 were pre-revenue 45% of the time, versus 21% for non-generative AI companies.

The Cannonball Effect of cross-over investors splashing into venture capital has evaporated. The Cannonball Effect cohort of 10 investment firms had a quarterly peak of 25 first-time V21 Seed, Series A, and Series B deals in 4Q21. The cohort had no such deals in 4Q23. This is a predictable outcome, and in fact, more than a few seasoned observers made exactly this prediction. History suggests they will be back; crossover investors entered early stage venture during the 2014–2015 and 2020–2021 market accelerations, and a similar pattern is likely in the next cycle.

The findings

V21 firms' deal volume

Last year, for the first time we reported on the trends in deal volume from the V21 dataset. Avid readers of the V21 study may recall that we typically do not do so, as deal volume figures in the V21 dataset are "unstable," at least initially due to under-reporting. For this reason we have historically focused on averages, medians and distributions on various figures of merit, as opposed to deal counts. However, in the current rapidly changing tech cycle, it is instructive to examine deal volume (despite the known imperfections in the "count" data).

Last year, we saw a remarkable decline in the V21 firms' deal volume over the previous four quarters. This year, the deal volume plateaued. The number of Seed deals remained unchanged from 62 in 4Q22 to 62 in 4Q23. The number of Series A's increased slightly from 30 in 4Q22 to 31 in 4Q23. The number of Series B's remained unchanged from 10 in 4Q22 to 10 in 4Q23. V21 firms' investment pace bottomed out in 2023 and in our view may be showing some weak signals of a return to (modest) growth, especially when you consider that 4Q23 deal counts are almost certainly under-reported as of this writing.

Generative AI venture capital deals continued to increase significantly in 2023. The percentage of first-time V21 deals in generative AI increased from 5.6% in 2022 to 15.1% in 2023. The percentage of Seeds increased from 4.7% in 2022 to 14.9% in 2023. The percentage of Series A's increased from 7.3% in 2022 to 10.6% in 2023. The percentage of Series B's increased from 4.5% in 2022 to 28.6% in 2023.

Cannonball Effect

We published in 2021 our study on the Cannonball Effect, in which non-traditional venture investors from the public and private equity markets invest large sums in early-stage venture capital and have an outsized impact on financing dynamics.

Last year, we saw a remarkable decline in the Cannonball Effect. This year, the Cannonball Effect evaporated completely. The Cannonball Effect cohort of 10 investment firms had no first-time Seeds, A's, and B's in 4Q23 — for the first time since 3Q19. By comparison, the cohort had 9 first-time Seeds, As, and Bs in 4Q22 and 25 first-time Seeds, As, and Bs in 4Q21.

Financing size

For early stage startup funding, we now return to core V21 dataset analysis.

We saw in last year's study a marked decrease on a quarterly basis in the median financing sizes of Series As and Series Bs. This year, we see the decrease on an annual basis. The median Series A financing was $17.2M in 2023, down 14% on a year-over-year basis, and the median Series B financing was $40M in 2023, down 7% on a year-over-year basis. Meanwhile, the median Seed financing was $5.2M in 2023, unchanged from the prior year.

The decrease in the Series A financing size drove a decrease in the Seed-to-A multiple to 3.3x in 2023, as compared to 3.9x in 2022. The A-to-B multiple remained relatively flat at 2.3x in 2023, as compared to 2.2x in 2022.

The market divergence is evident in the median financing sizes of generative AI vs. non-generative AI companies. Generative AI companies have median financing sizes 27% larger than non-generative AI companies at Seed, 6% larger at Series A, and 34% larger at Series B.

Jumbo Series A's

Last year, we discussed the increasing trend of $30M+ Series As. This year, with the slowdown in deal volume and median financing size, we see decreases in the numbers of $10M+ and $20M+ Series As and in the percentages of those size Series As out of all Series As.

The number of $10M+ Series As was 166 in 2023, representing 85% of all Series As in 2023. By comparison, the number was 331 in 2022, representing 88% of all Series As in 2022. The number of $20M+ Series As was 76 in 2023, representing 39% of all Series A's in 2023. By comparison, the number was 187 in 2022, representing 49% of all Series As in 2022.

But in another sign of the market divergence, the percentage of $30M+ Series As of all Series A's actually increased slightly in 2023. The number of $30M+ Series As was 37 in 2023, representing 19% of all Series As in 2023. By comparison, the number was 68 in 2022, representing 18% of all Series As in 2022. (For historical perspective, consider that the percentage of $30M+ Series As was 2% in 2010!) A large number of these $30M+ Series As were raised by generative AI companies. In some categories of generative AI, such as large model developers, the sheer capital intensity of these projects allowed founders to make the case for super-sized financings. Investor exuberance played a role as well — many were quietly scrambling to deploy the large pools of capital they had raised in frothier times.

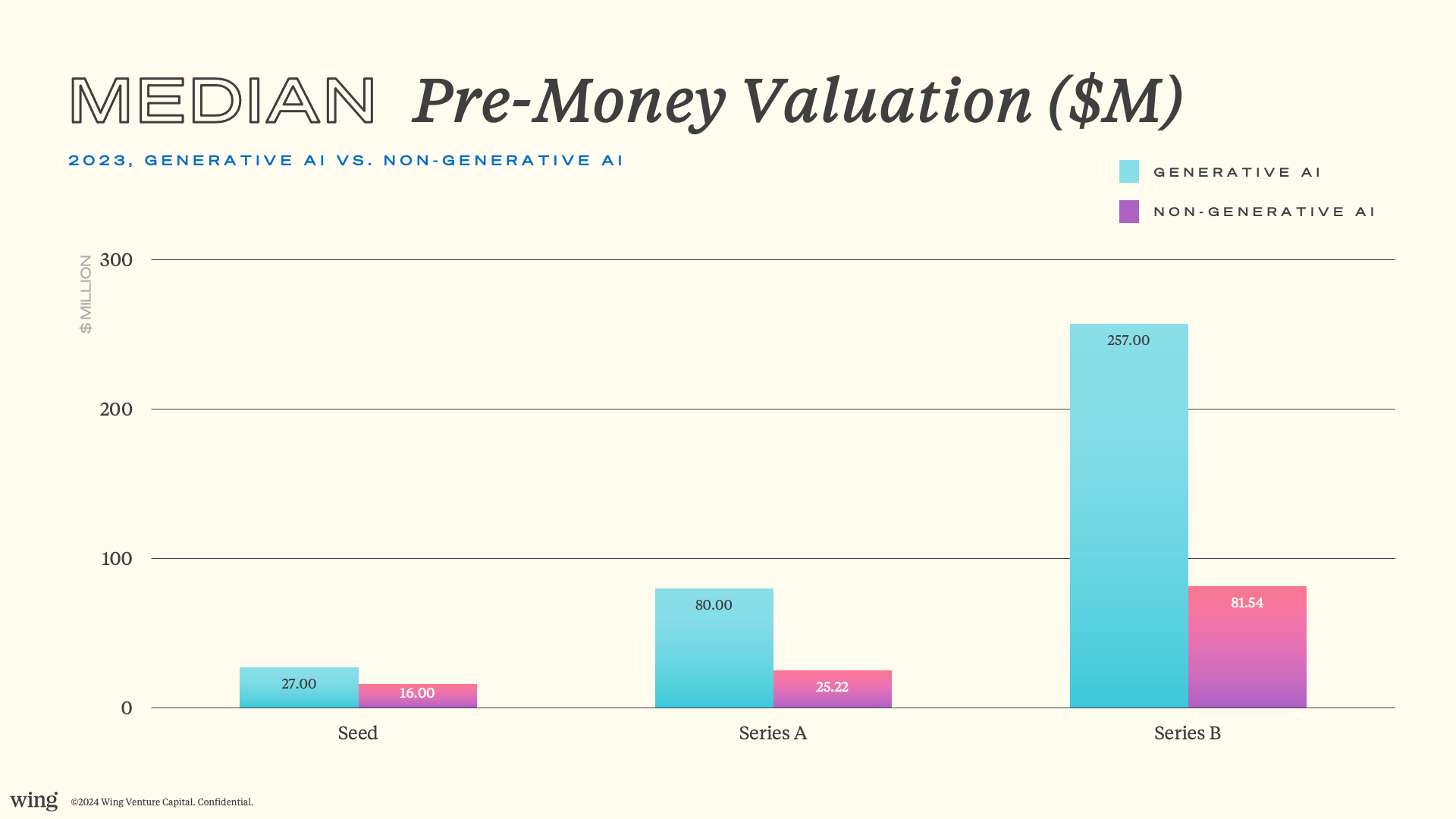

Pre-money valuation

As with financing sizes, pre-money valuations decreased for Series As and Series Bs in 2023. The median Series A pre-money valuation was $48M in 2023, down 20% from the prior year. The median Series B pre-money valuation was $160M in 2023, down 30% from the prior year.

The median seed round valuation was $17M in 2023, down 3% from $17.6M in 2022. The Seed financing characteristics are less affected, at least thus far, by the market downturn than the Series A and Series B financing characteristics. It is interesting to speculate as to why the seed valuations have held up more than the A's and B's. Perhaps it's as simple as "hope springs eternal"? More likely it is the higher percentage of on-trend generative AI companies in the newest cohort of startups.

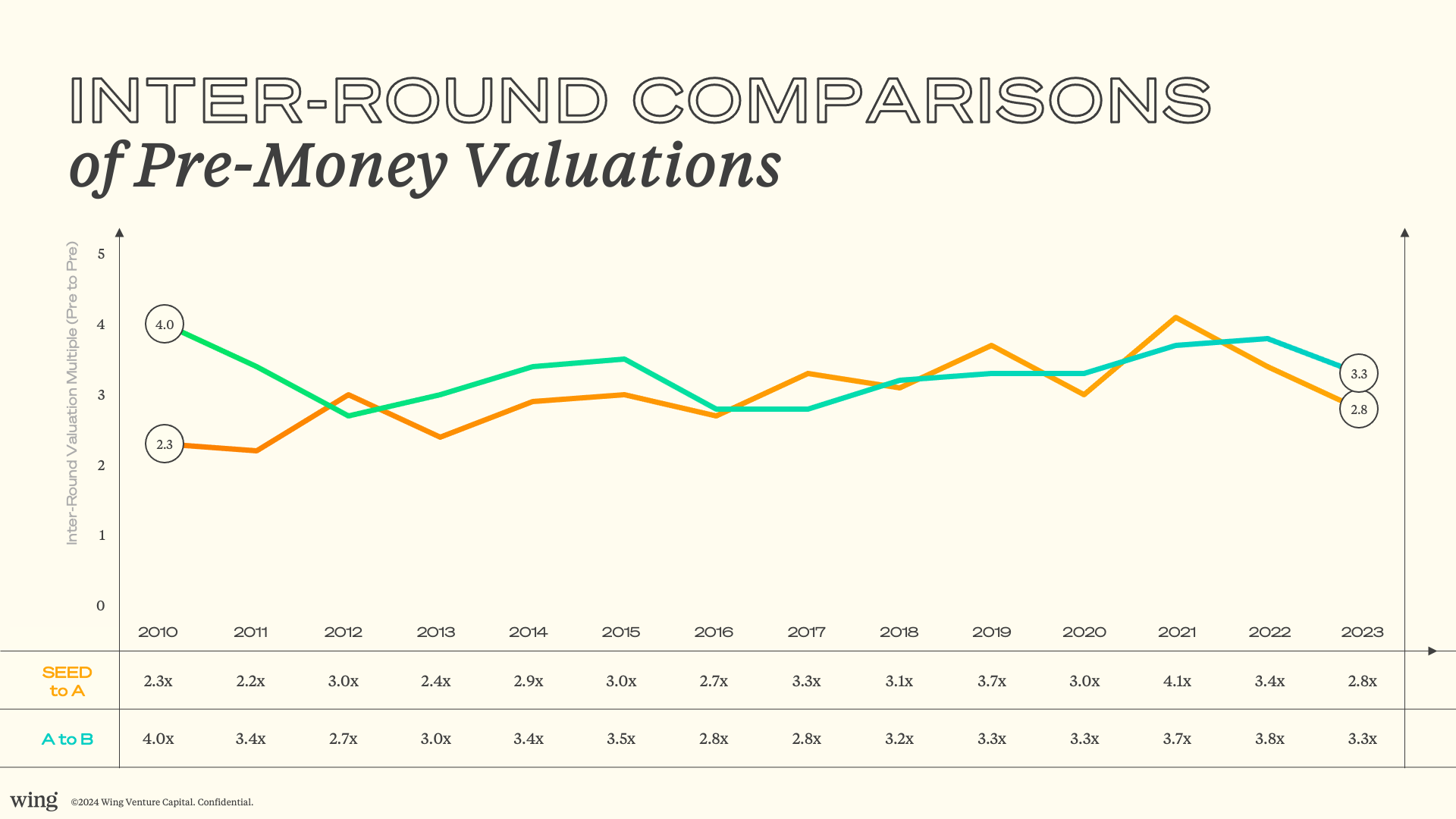

With the drying-up of the Cannonball Effect, we see a return to the "Rule of 3x," a long-term trend where the pre-money to pre-money multiple between rounds is approximately 3x. In 2023, the pre-money Seed to pre-money Series A was 2.8x, as compared to a recent high of 4.1x in 2021. The pre-money Series A to pre-money Series B was 3.3x in 2023, as compared to a recent high of 3.8x in 2022.

The market divergence is even more significant in pre-money valuations for generative AI companies. Generative AI companies have pre-money valuations 69% larger than non-generative AI companies at Seed, 217% larger at Series A, and 215% larger at Series B. Of course there is a correlation between the higher valuations and the larger round sizes for these companies.

Stage | generative AI median pre-money valuation premium vs. non-generative AI |

|---|---|

Seed | +69% |

Series A | +217% |

Series B | +215% |

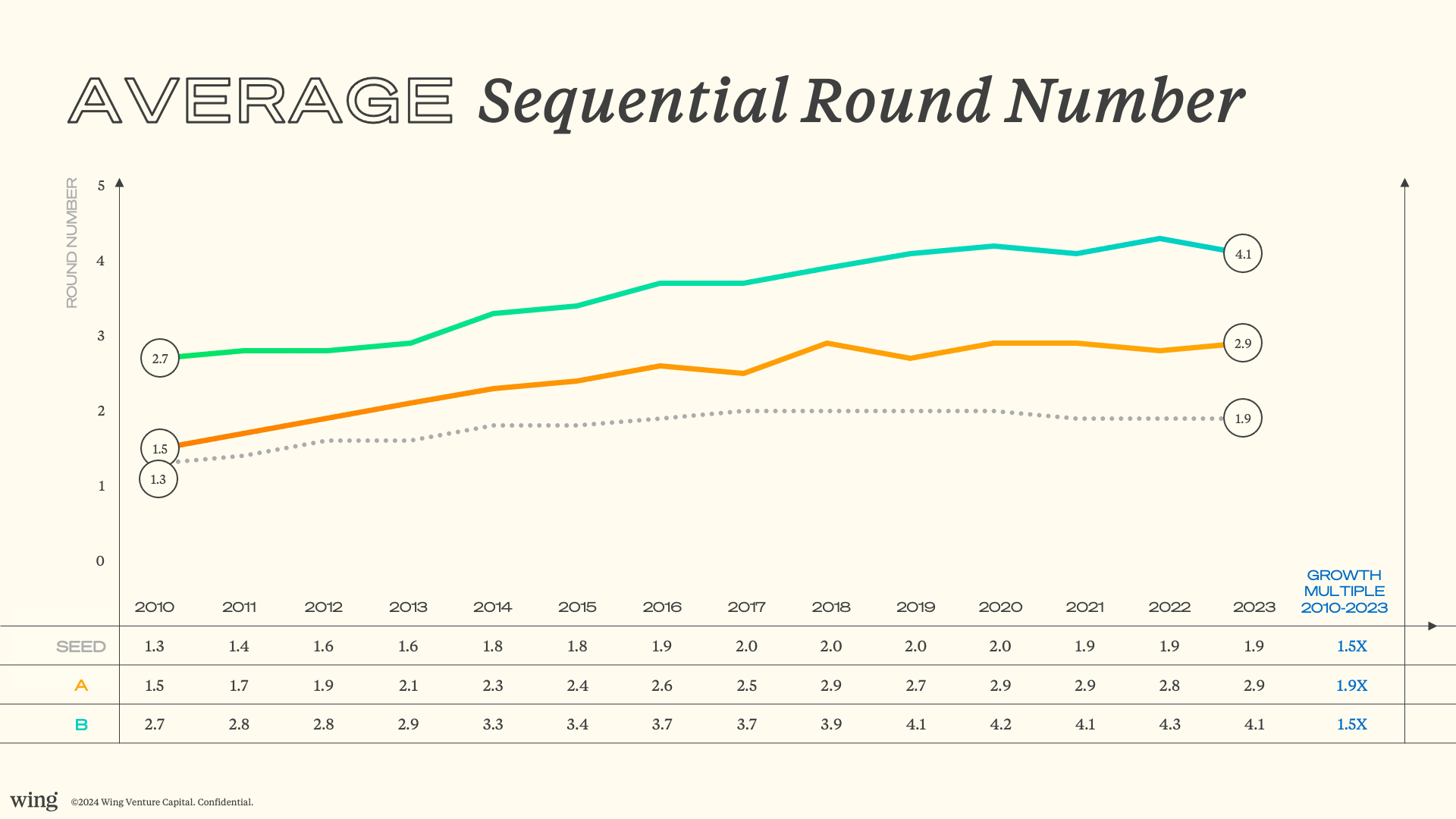

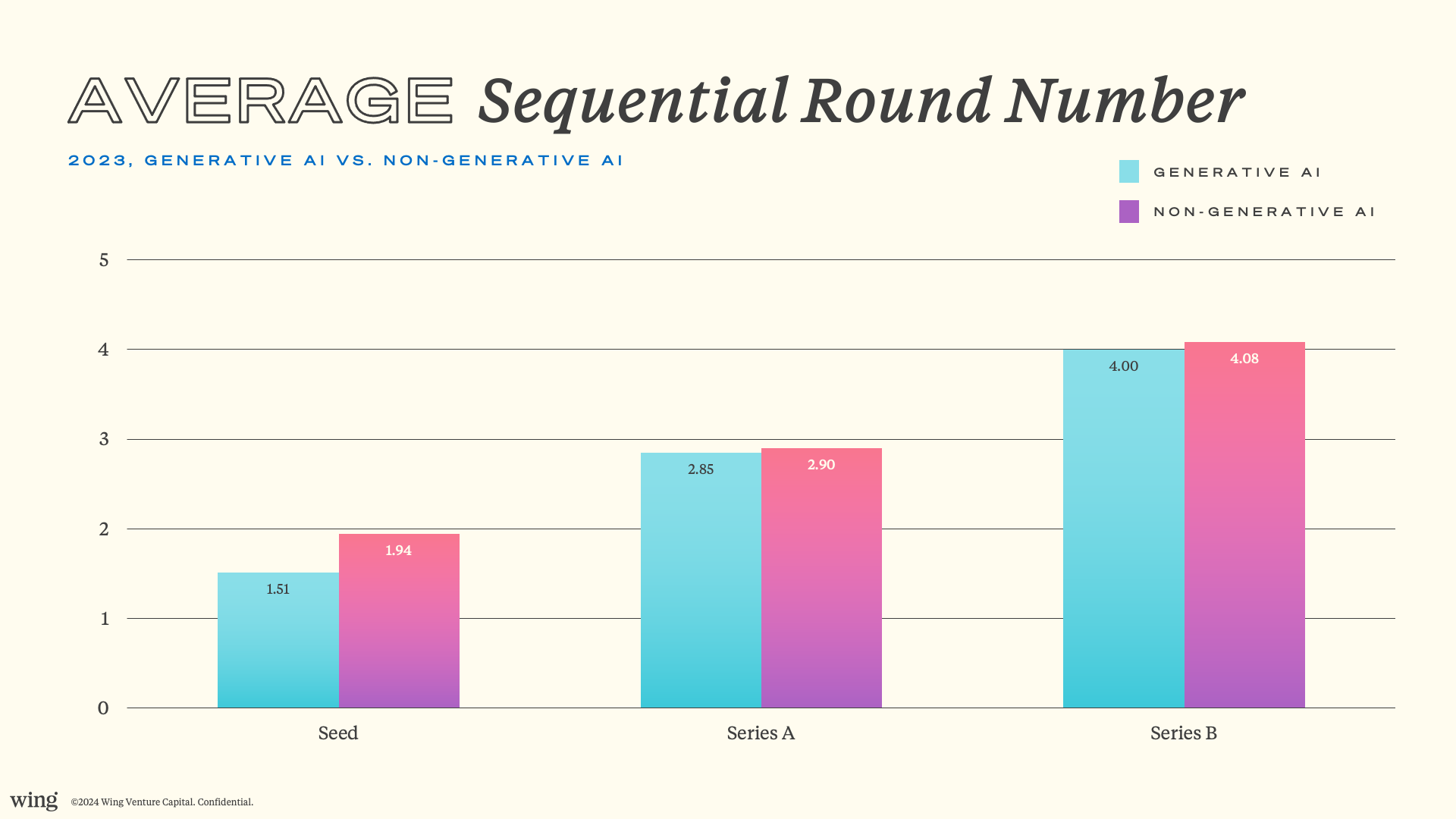

Round number

The average "sequential number of rounds" has leveled off for Seeds, Series As, and Series Bs. The average Seed financing was round number 1.9 in 2023 (i.e., it was basically that company's second financing), unchanged from the prior seven years. The average Series A financing was round number 2.9 in 2023, unchanged from the prior five years. The average Series B financing was round number 4.1 in 2023, relatively unchanged from the prior four years. V21 data shows the industry has settled on two Seed-style financings before the Series A, followed by the standard alphabetical progression.

Cumulative capital raised prior to round

Cumulative capital raised before a seed round spiked 56% in 2023, reaching an average of $1.4M, up from $0.9M in 2022 — a sharp acceleration driven in part by stacking simple agreements for future equity (SAFEs) as companies delayed major rounds. V21 companies raising Series As had raised an average of $7.0M in 2023, up 46% from 2022. And, V21 companies raising Series Bs had raised an average of $31.5M in 2023, up 13% from 2022. Companies may have delayed major financings when possible and tackedon additional capital through SAFE stacking. This pattern likely drove much of the increase in total capital raised prior to each round.

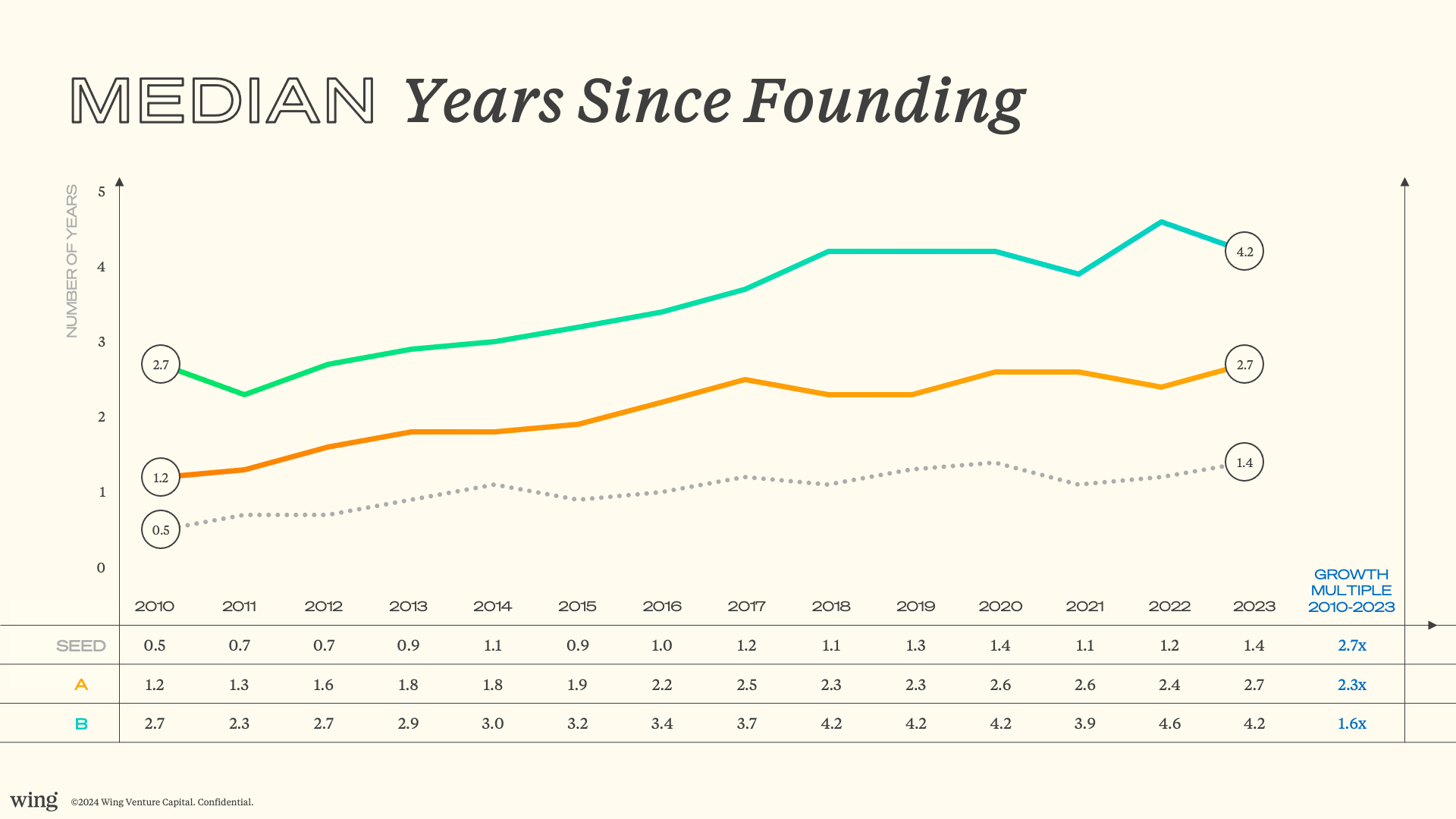

Years since founding

"Years since founding" returned to pre-Cannonball Effect levels in 2023. The median years since founding for Seeds was 1.4 in 2023, flat from 1.4 in 2020 and up from a low of 1.1 in 2021. The median years since founding for A's was 2.7 in 2023, relatively flat from 2.6 in 2020 and up from a low of 2.4 in 2022. The median years since founding for Bs was 4.2 in 2023, flat from 4.2 in 2020 and up from a low of 3.9 in 2021.

Seeds and Series As for generative AI companies have fewer years since founding than those non-generative AI companies. The median years since founding for Seeds in generative AI companies was 0.7 in 2023, as compared to 1.5 in non-generative AI companies. The median years since founding for A's in generative AI companies was 1.7 in 2023, as compared to 2.8 in non-generative AI companies. Once again, the relative youth of the generative AI group is most likely a reflection of these companies' greater need for capital as well as greater investor desire to provide it.

Revenue generation

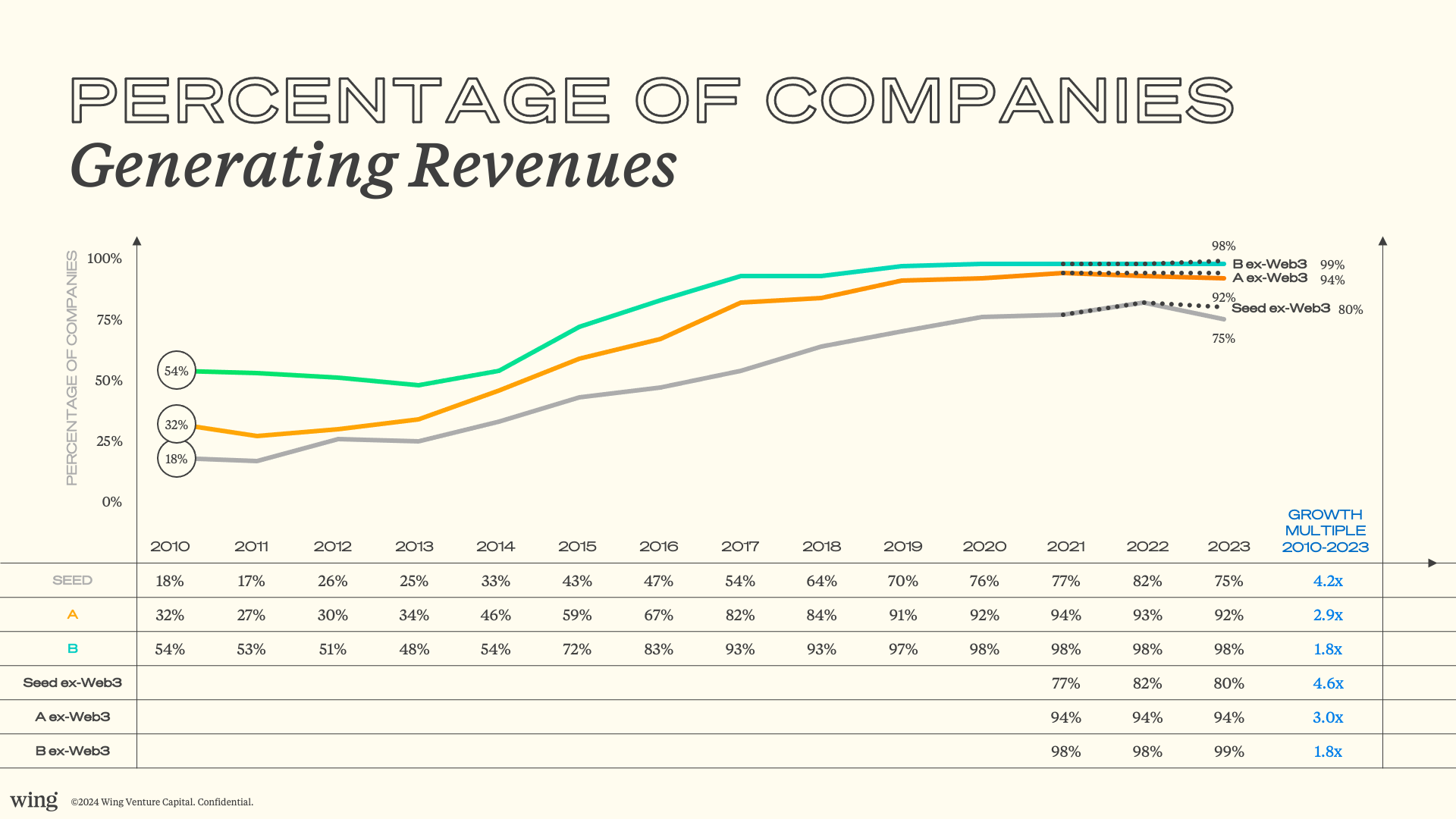

The proportion of companies that are revenue-generating for Seeds decreased noticeably from 2022 to 2023. 75% of companies raising Seed financings in 2023 were revenue generating, down from 82% in 2022. Meanwhile, the proportion of companies that are revenue-generating decreased slightly for Series As and remained flat for Series Bs. 92% of companies raising Series A financings in 2023 were revenue generating, slightly down from 93% in 2022. 98% of companies raising Series B financings in 2023 were revenue generating, unchanged from 98% in 2022.

The revenue data becomes clearer when viewed alongside the composition of V21 deal volume. As discussed earlier in this study, 14.9% of Seeds by V21 firms were in generative AI in 2023, up from 4.7% in 2022 and 4% in 2021. In addition, 12.6% of Seeds by V21 firms were in Web3 in 2023, down from 20.6% in 2022 but up from 9.6% in 2021.

We return to the V21 dataset to understand the characteristics of both generative AI and Web3 companies. As we discussed in last year's study, Web3 companies are more often pre-revenue than non-Web 3 companies. In addition, we see this year that generative AI companies are pre-revenue significantly more often than non-generative AI companies. 45% of the generative AI companies receiving Seed financings in 2023 were pre-revenue, and 28% of Web3 companies receiving Seed financings in 2023 were pre-revenue. By comparison, 20% of all other companies receiving Seed financings in 2023 were pre-revenue.

Time Machine analysis

As we introduced in prior studies, the cross-class analysis for "look-alikes" between current-era financings and preceding-era deals remains instructive. 2020 is a pivot point where "Seed is the new A" and "A is the new B".

This year's update:

Metric | 2023 Seed | 2010 Series A | 2023 Series A | 2010 Series B |

|---|---|---|---|---|

Pre-money valuation | $17M | $8.2M | $48M | $32.7M |

Financing size | $5.2M | $4.5M | $17.2M | $11M |

Sequential round number | 1.9 | 1.5 | 2.9 | 2.7 |

Methodology update

Each year, we update and re-examine the V21 dataset. We add a new year's worth of data, which impacts prior years' data due to the longitudinal financing histories of newly added V21 companies. To ensure data consistency, we re-download and re-run the entire dataset from PitchBook back to 2010. The 2023 V21 dataset includes 11,381 Seed, Series A, and Series B financings across 5,598 companies with at least one V21 venture capital investor.

This year, we also tagged the companies with generative AI vs. non-generative AI. As a note, the tagging process is imperfect. Some companies are obviously generative AI, whereas other companies, such as deep tech companies meeting the infrastructure requirements of AI workloads, may not be obvious. For our tagging, we reviewed 7 description fields in Pitchbook for keywords associated with generative AI.

A note on Series A's: The Series A figures throughout this study are not affected by growth equity financings labeled as Series A's. In our methodology, we manually remove those deals so that the V21 dataset includes venture-backed startups only and excludes mature bootstrapped companies and company spinouts.

A full recap of the V21 methodology is in the V21 2020 study.

Frequently asked questions

How much are AI startups raising compared to non-AI startups at seed?

In 2023, generative AI companies receiving seed financings from V21 firms had median round sizes 27% larger than non-generative AI companies. Their median pre-money valuations were 69% larger. At Series A, the valuation premium widened to 217%.

What is the median seed round valuation in 2023?

The median seed pre-money valuation among V21-backed companies was $17M in 2023, down just 3% from $17.6M in 2022. Seeds have been notably more resilient than later stages, where valuations fell 20--30%.

What happened to Series A deal sizes in 2023?

The median Series A financing was $17.2M in 2023, down 14% year over year. The median pre-money valuation fell 20% to $48M. The Seed-to-A multiple compressed from 3.9x in 2022 to 3.3x in 2023.

What is the Cannonball Effect and why does it matter for early-stage startup funding?

The Cannonball Effect describes the period when crossover investors from public and private equity markets made large bets in early-stage venture, driving up valuations and deal sizes. By Q4 2023, this cohort had zero first-time seed, Series A, or Series B investments -- down from 25 per quarter at the 2021 peak. Their withdrawal has normalized inter-round valuation multiples back toward the historical "Rule of 3x."

How are generative AI startups different from other early-stage companies?

In 2023, generative AI companies receiving seed funding had a median age of just 0.7 years since founding, versus 1.5 years for non-generative AI companies. 45% of generative AI seed-stage companies were pre-revenue, compared to 21% of their peers. Investors are funding these companies earlier and at a higher conviction level than at any prior stage of the AI cycle.

Conclusion

Wing was founded in 2013 on the belief that the combined action of Data, Mobility, and the Cloud would establish a new paradigm in business technology. That thesis proved prescient — Snowflake, Cohesity, Gong, and Pinecone each built category-defining businesses on that foundation over the following decade. As the "DMC" shift played out, it established the preconditions for the next, even more powerful super-cycle: the AI-first transformation of business.

We expect the market divergence that we see today to reconverge at some point. Currently even good companies that aren't sufficiently associated with the "new new thing" have a hard time getting financing. However, just as no one now distinguishes "cloud companies" from technology companies — a shift that played out over roughly a decade after AWS launched in 2006 — AI will follow a similar arc. Within the next cycle, AI capabilities will be a baseline expectation for any technology company, not a distinguishing label. For founders building AI-first companies, the AI startup funding environment in 2023 reflects exceptional investor conviction — but also the early pressure points of a market still sorting itself out.

In the meantime, there will be a highly imperfect sorting as founders and companies scramble to reset their products, technologies, and offerings. This will result in some collateral damage for more than a few prior-paradigm companies on the wrong side of the sort. This sorting also creates a real opening for founders who build with the new paradigm from the start to establish enduring companies.

Let us know your thoughts and reactions.

Peter Wagner, Co-Founder & General Partner, Wing Venture Capital

Rajeev Chand, Head of Research, Wing Venture Capital

.avif)